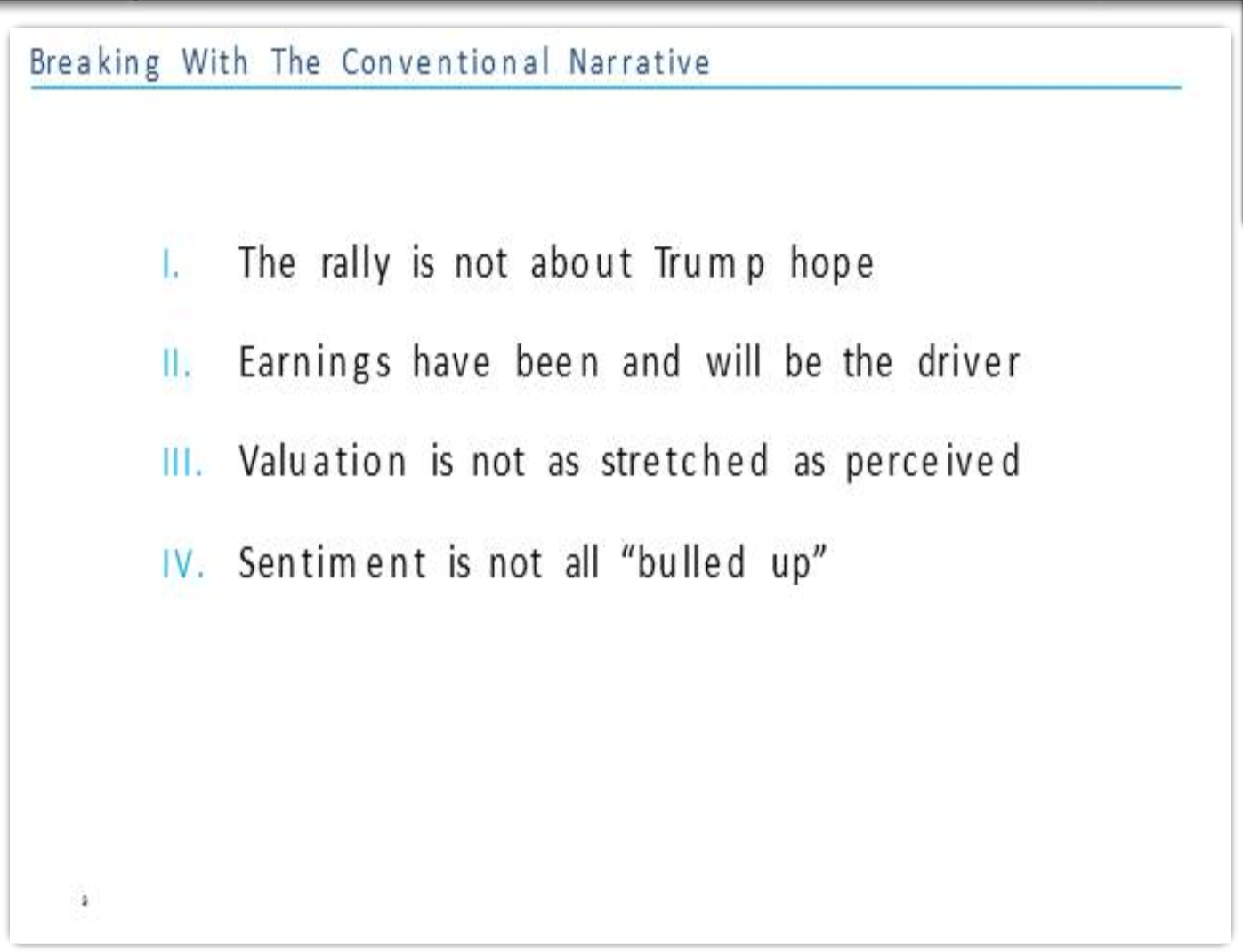

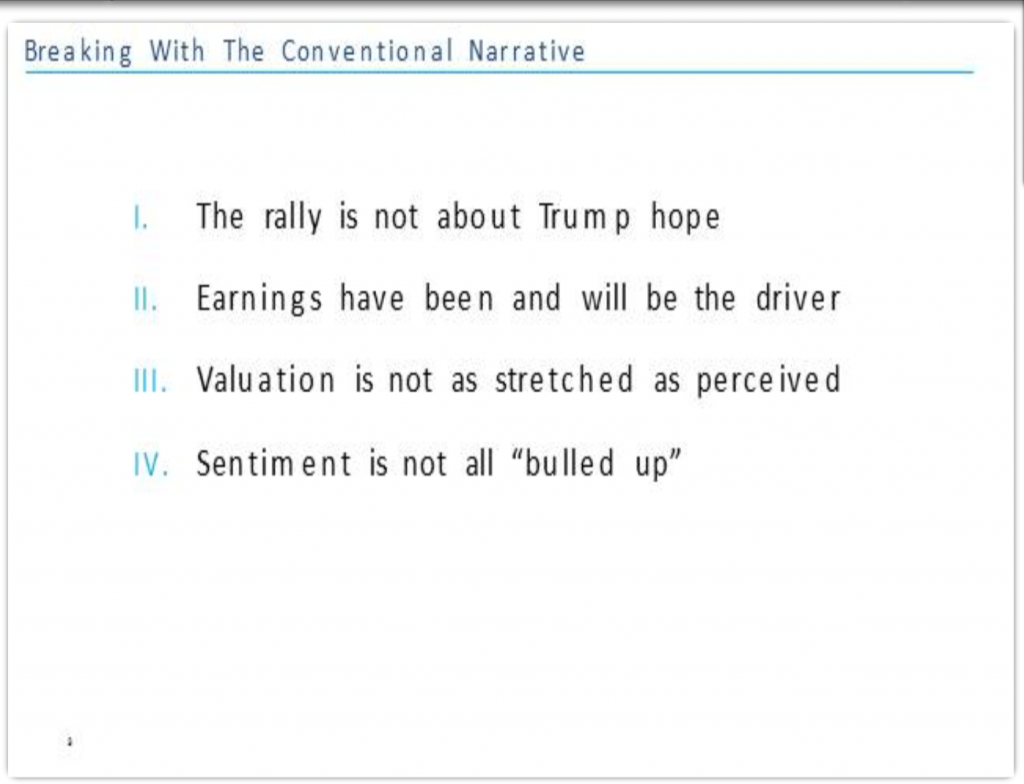

Oh, it was a rally alright. But Trump, arguably, had little to do with it.

Investors are not as bullish, despite the momentum since the election in November.

“I’ve talked to at least 180 institutional clients face-to-face over the past four weeks and I think I’ve met seven bulls with about 30 or 40 outright bears,” Levkovich says.

Worth noting, he is not expecting a major correction. He is not particularly bearish. Nor does he think the rally is over. Their 2017 target for the S&P 500 is 2,425 (we’re at 2,352 as of April 5). For the Dow, it’s 21,000 (now 20,468).

Investors have been waiting for an earnings rebound for some time. They’ve got it. The third quarter of last year was particularly strong. So much for the earnings recession some in the market have been talking about over the last year or two. But if you take that view, that corporations just weren’t bringing home the bacon, then consider throwing that baby out with the bath water for a second. We have not been in an earnings recession. We have been in an energy depression, Levkovich says about the collapse of oil which took place in 2014 and drove crude all the way down to the $30s last February.

With energy prices looking better, Citi Research now assumes S&P 500 estimated earnings for the year are $131 earnings per share, up 8.7% from 2016. Half of that is coming from energy firms, and the numbers could move higher if the first quarter looks good. “We have high conviction of that,” he says.

Has the Trump rally, or as Citi might consider it, a faux Trump rally, pushed prices through the roof? Yes. For 10-year Treasury bonds. “They look stupid,” says Levkovich.

Historically, when inflation is under 4%, securities are highly valued. But it’s when inflation rises over 4% that valuation becomes a major problem. For Citi, inflation hits 3% –maybe — this year. In other words, they’re not worried about valuation all that much.

Citi has this well-known Panic/Euphoria Model, which they call the “Other P/E”. According to their model, which encompasses nine different metrics and portfolio asset allocation, the “other P/E” is neutral. No panic. No euphoria either, believe it or not.

“We are not seeing wild bullishness out there. People don’t have great conviction one way or the other,” he says. “I don’t see this. Maybe some guys do, but I am not hearing it.”

Citi’s research team recommends an overweight in banks, capital goods companies, consumer services sector, diversified financials, media and, of course, energy. They are not fans of the automotive industry, food and beverage, software services firms, telecos and even big pharma and biotech. Those are recommended underweights. He was not company specific.

Levkovich takes a rather professorial view of the markets, spending the better part of the hour-long seminar trying to convince investors that the Trump rally is, um, “fake news”. Inflation was on the upswing now for 13 months straight. Earnings were improving before the election. Capital spending was moving higher.

“Irrespective of what goes on in Washington DC, the earnings trend is going to continue. I don’t have to be prophetic to look at some of these charts and see that it is going to move higher in the next few months,” he says of lead indicators like NFIB small business employment and the Wage Growth Tracker from the Atlanta Federal Reserve Bank.

Indicators like that give investors a sense of what the pizza shop and the auto mechanics are thinking about hiring. It’s where America lives. That’s the gauge to forecasting whether or not rallies have a leg to stand on. There’s still a pick-up in wage gains and hiring intentions. Wage inflation is absolutely coming.

“I don’t know the future. It’s about examining how things have looked historically, and establishing a very consistent path. It’s certainly not about watching the news flow out of DC,” he says.

The Citi webinar is available for replay online.

Oh, it was a rally alright. But Trump, arguably, had little to do with it.

Investors are not as bullish, despite the momentum since the election in November.

“I’ve talked to at least 180 institutional clients face-to-face over the past four weeks and I think I’ve met seven bulls with about 30 or 40 outright bears,” Levkovich says.

Worth noting, he is not expecting a major correction. He is not particularly bearish. Nor does he think the rally is over. Their 2017 target for the S&P 500 is 2,425 (we’re at 2,352 as of April 5). For the Dow, it’s 21,000 (now 20,468).

Investors have been waiting for an earnings rebound for some time. They’ve got it. The third quarter of last year was particularly strong. So much for the earnings recession some in the market have been talking about over the last year or two. But if you take that view, that corporations just weren’t bringing home the bacon, then consider throwing that baby out with the bath water for a second. We have not been in an earnings recession. We have been in an energy depression, Levkovich says about the collapse of oil which took place in 2014 and drove crude all the way down to the $30s last February.

With energy prices looking better, Citi Research now assumes S&P 500 estimated earnings for the year are $131 earnings per share, up 8.7% from 2016. Half of that is coming from energy firms, and the numbers could move higher if the first quarter looks good. “We have high conviction of that,” he says.

Has the Trump rally, or as Citi might consider it, a faux Trump rally, pushed prices through the roof? Yes. For 10-year Treasury bonds. “They look stupid,” says Levkovich.

Historically, when inflation is under 4%, securities are highly valued. But it’s when inflation rises over 4% that valuation becomes a major problem. For Citi, inflation hits 3% –maybe — this year. In other words, they’re not worried about valuation all that much.

Citi has this well-known Panic/Euphoria Model, which they call the “Other P/E”. According to their model, which encompasses nine different metrics and portfolio asset allocation, the “other P/E” is neutral. No panic. No euphoria either, believe it or not.

“We are not seeing wild bullishness out there. People don’t have great conviction one way or the other,” he says. “I don’t see this. Maybe some guys do, but I am not hearing it.”

Citi’s research team recommends an overweight in banks, capital goods companies, consumer services sector, diversified financials, media and, of course, energy. They are not fans of the automotive industry, food and beverage, software services firms, telecos and even big pharma and biotech. Those are recommended underweights. He was not company specific.

Levkovich takes a rather professorial view of the markets, spending the better part of the hour-long seminar trying to convince investors that the Trump rally is, um, “fake news”. Inflation was on the upswing now for 13 months straight. Earnings were improving before the election. Capital spending was moving higher.

“Irrespective of what goes on in Washington DC, the earnings trend is going to continue. I don’t have to be prophetic to look at some of these charts and see that it is going to move higher in the next few months,” he says of lead indicators like NFIB small business employment and the Wage Growth Tracker from the Atlanta Federal Reserve Bank.

Indicators like that give investors a sense of what the pizza shop and the auto mechanics are thinking about hiring. It’s where America lives. That’s the gauge to forecasting whether or not rallies have a leg to stand on. There’s still a pick-up in wage gains and hiring intentions. Wage inflation is absolutely coming.

“I don’t know the future. It’s about examining how things have looked historically, and establishing a very consistent path. It’s certainly not about watching the news flow out of DC,” he says.

The Citi webinar is available for replay online. Citi Says This Is No Trump Rally

Back in December, as markets were rolling into the Year of The Donald, a repeal and replace of Obamacare coupled with corporate tax cuts were everyone’s favorite bet to drive markets higher. Wall Street traders put on their Dow 20,000 hats, which quickly gave way to their Dow 21,000 hats. Trump complimented himself for the rally.

Not this guy: Citibank’s chief U.S. equity strategist Tobias Levkovich had doubts. Then again, he’s Canadian. He has a different view of things. It also helps that he is somewhat of an obvious financials and accounting nerd. He likes the math. He likes to do his homework. And his homework told him that it was “premature to build any such tax plan into forecasts.” Single factor dynamics are “out and out dangerous” for investors, he said.

RIA Channel ran a webinar with Citi on March 29 to discuss the “Trump rally”, which – if you believe in the Trump rally narrative – is now running out of steam. For Citi, it never really was a Trump rally anyway.

Oh, it was a rally alright. But Trump, arguably, had little to do with it.

Investors are not as bullish, despite the momentum since the election in November.

“I’ve talked to at least 180 institutional clients face-to-face over the past four weeks and I think I’ve met seven bulls with about 30 or 40 outright bears,” Levkovich says.

Worth noting, he is not expecting a major correction. He is not particularly bearish. Nor does he think the rally is over. Their 2017 target for the S&P 500 is 2,425 (we’re at 2,352 as of April 5). For the Dow, it’s 21,000 (now 20,468).

Investors have been waiting for an earnings rebound for some time. They’ve got it. The third quarter of last year was particularly strong. So much for the earnings recession some in the market have been talking about over the last year or two. But if you take that view, that corporations just weren’t bringing home the bacon, then consider throwing that baby out with the bath water for a second. We have not been in an earnings recession. We have been in an energy depression, Levkovich says about the collapse of oil which took place in 2014 and drove crude all the way down to the $30s last February.

With energy prices looking better, Citi Research now assumes S&P 500 estimated earnings for the year are $131 earnings per share, up 8.7% from 2016. Half of that is coming from energy firms, and the numbers could move higher if the first quarter looks good. “We have high conviction of that,” he says.

Has the Trump rally, or as Citi might consider it, a faux Trump rally, pushed prices through the roof? Yes. For 10-year Treasury bonds. “They look stupid,” says Levkovich.

Historically, when inflation is under 4%, securities are highly valued. But it’s when inflation rises over 4% that valuation becomes a major problem. For Citi, inflation hits 3% –maybe — this year. In other words, they’re not worried about valuation all that much.

Citi has this well-known Panic/Euphoria Model, which they call the “Other P/E”. According to their model, which encompasses nine different metrics and portfolio asset allocation, the “other P/E” is neutral. No panic. No euphoria either, believe it or not.

“We are not seeing wild bullishness out there. People don’t have great conviction one way or the other,” he says. “I don’t see this. Maybe some guys do, but I am not hearing it.”

Citi’s research team recommends an overweight in banks, capital goods companies, consumer services sector, diversified financials, media and, of course, energy. They are not fans of the automotive industry, food and beverage, software services firms, telecos and even big pharma and biotech. Those are recommended underweights. He was not company specific.

Levkovich takes a rather professorial view of the markets, spending the better part of the hour-long seminar trying to convince investors that the Trump rally is, um, “fake news”. Inflation was on the upswing now for 13 months straight. Earnings were improving before the election. Capital spending was moving higher.

“Irrespective of what goes on in Washington DC, the earnings trend is going to continue. I don’t have to be prophetic to look at some of these charts and see that it is going to move higher in the next few months,” he says of lead indicators like NFIB small business employment and the Wage Growth Tracker from the Atlanta Federal Reserve Bank.

Indicators like that give investors a sense of what the pizza shop and the auto mechanics are thinking about hiring. It’s where America lives. That’s the gauge to forecasting whether or not rallies have a leg to stand on. There’s still a pick-up in wage gains and hiring intentions. Wage inflation is absolutely coming.

“I don’t know the future. It’s about examining how things have looked historically, and establishing a very consistent path. It’s certainly not about watching the news flow out of DC,” he says.

The Citi webinar is available for replay online.

Oh, it was a rally alright. But Trump, arguably, had little to do with it.

Investors are not as bullish, despite the momentum since the election in November.

“I’ve talked to at least 180 institutional clients face-to-face over the past four weeks and I think I’ve met seven bulls with about 30 or 40 outright bears,” Levkovich says.

Worth noting, he is not expecting a major correction. He is not particularly bearish. Nor does he think the rally is over. Their 2017 target for the S&P 500 is 2,425 (we’re at 2,352 as of April 5). For the Dow, it’s 21,000 (now 20,468).

Investors have been waiting for an earnings rebound for some time. They’ve got it. The third quarter of last year was particularly strong. So much for the earnings recession some in the market have been talking about over the last year or two. But if you take that view, that corporations just weren’t bringing home the bacon, then consider throwing that baby out with the bath water for a second. We have not been in an earnings recession. We have been in an energy depression, Levkovich says about the collapse of oil which took place in 2014 and drove crude all the way down to the $30s last February.

With energy prices looking better, Citi Research now assumes S&P 500 estimated earnings for the year are $131 earnings per share, up 8.7% from 2016. Half of that is coming from energy firms, and the numbers could move higher if the first quarter looks good. “We have high conviction of that,” he says.

Has the Trump rally, or as Citi might consider it, a faux Trump rally, pushed prices through the roof? Yes. For 10-year Treasury bonds. “They look stupid,” says Levkovich.

Historically, when inflation is under 4%, securities are highly valued. But it’s when inflation rises over 4% that valuation becomes a major problem. For Citi, inflation hits 3% –maybe — this year. In other words, they’re not worried about valuation all that much.

Citi has this well-known Panic/Euphoria Model, which they call the “Other P/E”. According to their model, which encompasses nine different metrics and portfolio asset allocation, the “other P/E” is neutral. No panic. No euphoria either, believe it or not.

“We are not seeing wild bullishness out there. People don’t have great conviction one way or the other,” he says. “I don’t see this. Maybe some guys do, but I am not hearing it.”

Citi’s research team recommends an overweight in banks, capital goods companies, consumer services sector, diversified financials, media and, of course, energy. They are not fans of the automotive industry, food and beverage, software services firms, telecos and even big pharma and biotech. Those are recommended underweights. He was not company specific.

Levkovich takes a rather professorial view of the markets, spending the better part of the hour-long seminar trying to convince investors that the Trump rally is, um, “fake news”. Inflation was on the upswing now for 13 months straight. Earnings were improving before the election. Capital spending was moving higher.

“Irrespective of what goes on in Washington DC, the earnings trend is going to continue. I don’t have to be prophetic to look at some of these charts and see that it is going to move higher in the next few months,” he says of lead indicators like NFIB small business employment and the Wage Growth Tracker from the Atlanta Federal Reserve Bank.

Indicators like that give investors a sense of what the pizza shop and the auto mechanics are thinking about hiring. It’s where America lives. That’s the gauge to forecasting whether or not rallies have a leg to stand on. There’s still a pick-up in wage gains and hiring intentions. Wage inflation is absolutely coming.

“I don’t know the future. It’s about examining how things have looked historically, and establishing a very consistent path. It’s certainly not about watching the news flow out of DC,” he says.

The Citi webinar is available for replay online.

Oh, it was a rally alright. But Trump, arguably, had little to do with it.

Investors are not as bullish, despite the momentum since the election in November.

“I’ve talked to at least 180 institutional clients face-to-face over the past four weeks and I think I’ve met seven bulls with about 30 or 40 outright bears,” Levkovich says.

Worth noting, he is not expecting a major correction. He is not particularly bearish. Nor does he think the rally is over. Their 2017 target for the S&P 500 is 2,425 (we’re at 2,352 as of April 5). For the Dow, it’s 21,000 (now 20,468).

Investors have been waiting for an earnings rebound for some time. They’ve got it. The third quarter of last year was particularly strong. So much for the earnings recession some in the market have been talking about over the last year or two. But if you take that view, that corporations just weren’t bringing home the bacon, then consider throwing that baby out with the bath water for a second. We have not been in an earnings recession. We have been in an energy depression, Levkovich says about the collapse of oil which took place in 2014 and drove crude all the way down to the $30s last February.

With energy prices looking better, Citi Research now assumes S&P 500 estimated earnings for the year are $131 earnings per share, up 8.7% from 2016. Half of that is coming from energy firms, and the numbers could move higher if the first quarter looks good. “We have high conviction of that,” he says.

Has the Trump rally, or as Citi might consider it, a faux Trump rally, pushed prices through the roof? Yes. For 10-year Treasury bonds. “They look stupid,” says Levkovich.

Historically, when inflation is under 4%, securities are highly valued. But it’s when inflation rises over 4% that valuation becomes a major problem. For Citi, inflation hits 3% –maybe — this year. In other words, they’re not worried about valuation all that much.

Citi has this well-known Panic/Euphoria Model, which they call the “Other P/E”. According to their model, which encompasses nine different metrics and portfolio asset allocation, the “other P/E” is neutral. No panic. No euphoria either, believe it or not.

“We are not seeing wild bullishness out there. People don’t have great conviction one way or the other,” he says. “I don’t see this. Maybe some guys do, but I am not hearing it.”

Citi’s research team recommends an overweight in banks, capital goods companies, consumer services sector, diversified financials, media and, of course, energy. They are not fans of the automotive industry, food and beverage, software services firms, telecos and even big pharma and biotech. Those are recommended underweights. He was not company specific.

Levkovich takes a rather professorial view of the markets, spending the better part of the hour-long seminar trying to convince investors that the Trump rally is, um, “fake news”. Inflation was on the upswing now for 13 months straight. Earnings were improving before the election. Capital spending was moving higher.

“Irrespective of what goes on in Washington DC, the earnings trend is going to continue. I don’t have to be prophetic to look at some of these charts and see that it is going to move higher in the next few months,” he says of lead indicators like NFIB small business employment and the Wage Growth Tracker from the Atlanta Federal Reserve Bank.

Indicators like that give investors a sense of what the pizza shop and the auto mechanics are thinking about hiring. It’s where America lives. That’s the gauge to forecasting whether or not rallies have a leg to stand on. There’s still a pick-up in wage gains and hiring intentions. Wage inflation is absolutely coming.

“I don’t know the future. It’s about examining how things have looked historically, and establishing a very consistent path. It’s certainly not about watching the news flow out of DC,” he says.

The Citi webinar is available for replay online.